The map shows overall economic well-being scores.

The map shows overall economic well-being scores.

.

Income and wealth are an important aspect of opportunity. Less generational wealth can impact a family's ability to pay for higher education or start a business. Not being able to access and build wealth in these and other ways continues to widen the wealth gap.

The Opportunity Index measures economic well-being using three measures. These are homeownership rates, child poverty, and access to financial institutions.

The Opportunity Index measures economic well-being using three measures. These are homeownership rates, child poverty, and access to financial institutions.

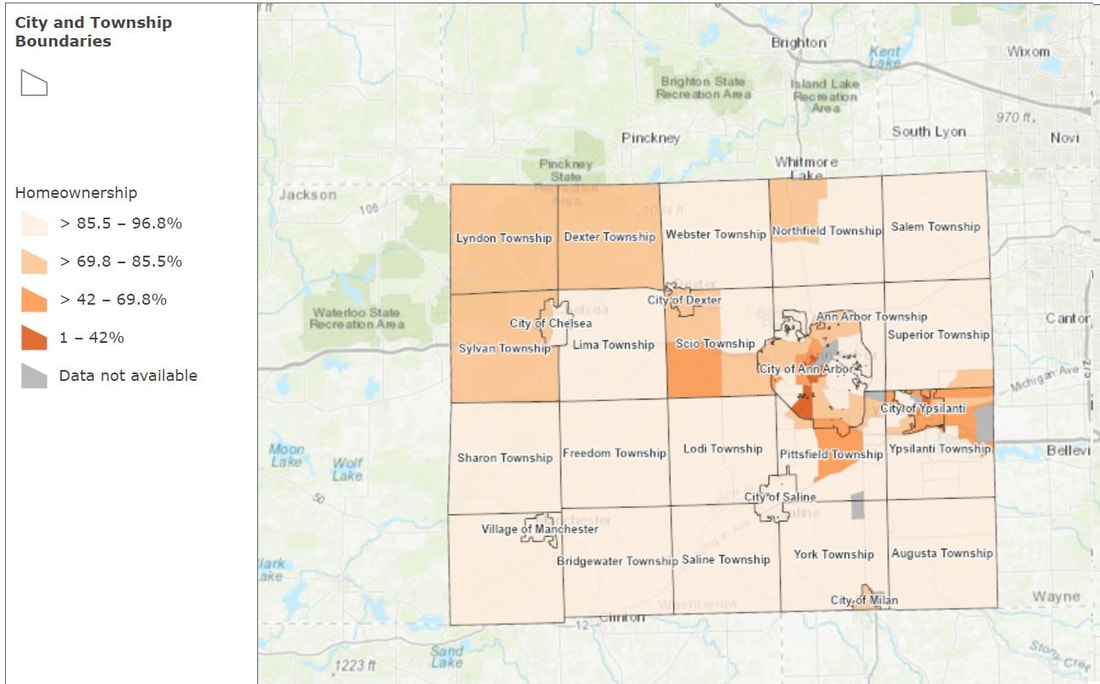

Homeownership Rates

The map shows the homeownership rate in each census tract.

Wealth is closely connected to homeownership. People of color have not had the opportunity to accumulate and pass along wealth through housing the same way white people have. This is due to the impact of redlining and other exclusionary housing practices. These practices included forcing people of color into specific neighborhoods and denying them mortgages to buy homes. Those segregated areas had lower property values and often experienced disinvestment. Thus, even if families of color were able to buy a home, it would be worth less, limiting their ability to accumulate wealth.

While the Fair Housing Act of 1968 made many of these practices illegal, their impact continues. Residential segregation and homeownership disparities are still present in our community.

Black homeowners also were disproportionately affected by the foreclosure crisis of the late-2000s. The Great Recession resulted in a 47.6% loss of wealth for black households compared to an overall loss of 28.5% for all U.S. families.

While not every household has homeownership as a goal, people of color have often not even had the option of making this a goal.

While the Fair Housing Act of 1968 made many of these practices illegal, their impact continues. Residential segregation and homeownership disparities are still present in our community.

Black homeowners also were disproportionately affected by the foreclosure crisis of the late-2000s. The Great Recession resulted in a 47.6% loss of wealth for black households compared to an overall loss of 28.5% for all U.S. families.

While not every household has homeownership as a goal, people of color have often not even had the option of making this a goal.

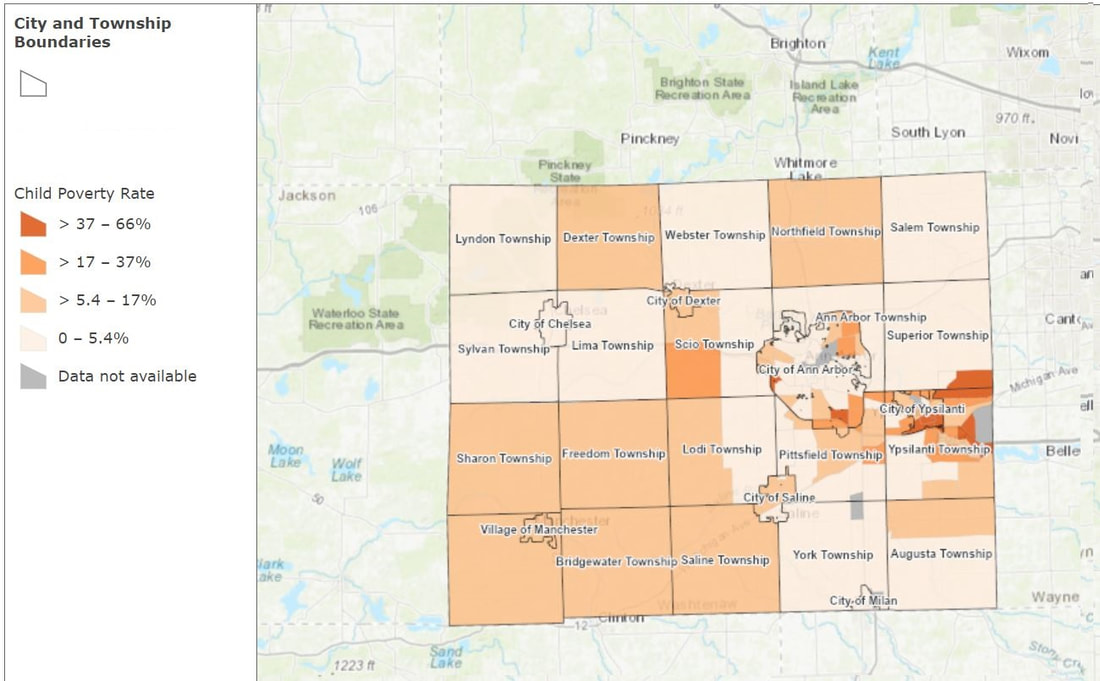

Child Poverty Rate

The map shows the percentage of children under the age of 18 living in households in poverty.

Growing up in poverty can have a negative effect on children's social, emotional, and cognitive development. It also can impact their health, behavior, and educational outcomes. Childhood poverty is most prevalent on the east side of Washtenaw County. This is the result of longstanding residential and racial segregation.

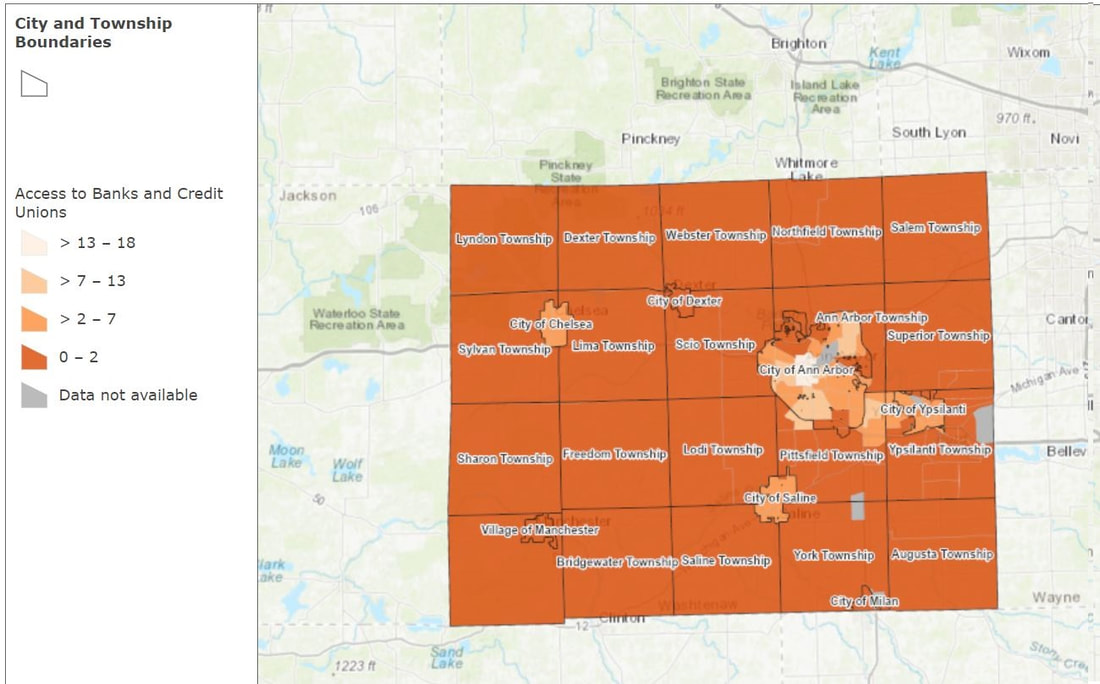

Access to Banks and Credit Unions

The map shows the number of banks and credit unions within a 1-mile radius of the center of the census tract.

Access to financial institutions is another measure of economic well-being. High-poverty areas often lack traditional financial institutions. Instead, these communities often only have access only to predatory, high-cost financial products (e.g., payday loans). This makes it more difficult for families to improve their financial situations.